- INTRODUCTION

The main objectives of accounting reporting requirements are to inform investors in capital markets, provide an overview of past transactions, and improve corporate governance. It is of paramount importance to streamline these requirements so that they can achieve their aims while minimizing the administrative burden on companies.

- RATIONALE?

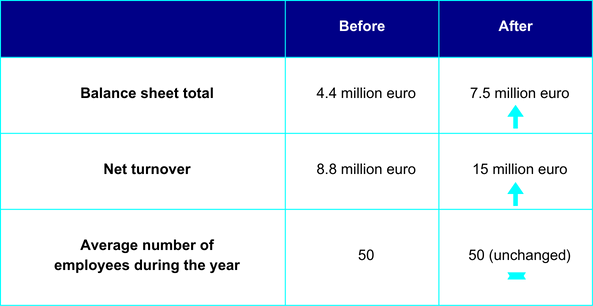

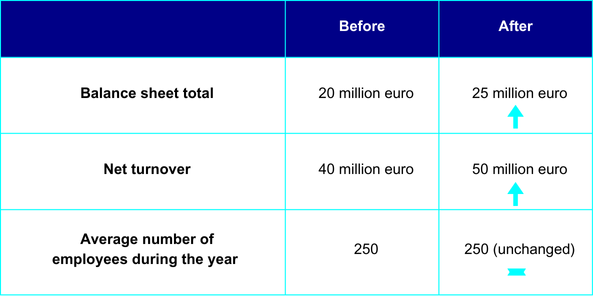

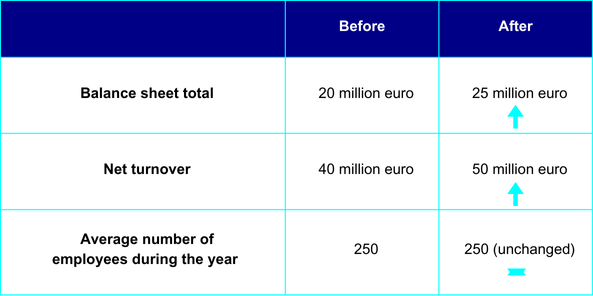

The figures provided by Eurostat indicate cumulative inflation over a period of around ten years (1st January 2013 to 31 March 2023) of around 24.3% in the eurozone and over 27% in the European Union as a whole. In addition, the high inflation observed in 2021 and 2022 has led the Commission to review the financial criteria determining the size category of companies with a view to re-evaluating them, resulting in an adjustment of 25%, which it has deemed necessary, and to round up the thresholds for determining the category of companies and groups.

- EFFECT?

This increase in thresholds will lead to a re-categorisation of certain large companies as medium-sized, exempting them from publishing sustainability information. At the same time, some medium-sized companies will become small companies, exempting them from having their accounts audited by a statutory auditor. As for groups, some will fall outside the criteria and will be exempt from publishing consolidated accounts.

- AMENDMENTS?

- The law of 10 August 1915 concerning commercial companies, as amended:

Article 1711-4 stating the rule concerning the obligation of parent companies to draw up consolidated accounts and a consolidated management report, will be amended as follows:

-

- The law of 19 December 2002 on the register of commerce and companies and the accounting and annual acounts of undertakings

Article 35 determining the criteria for the layout of the balance sheet, will be amended as follows:

Article 47 determining the criteria for the layout of the profit and loss accounts, will be amended as follows:

- AS OF WHEN?

In compliance with the option offered by the Commission, Luxembourg has decided of making these criteria applicable for financial years beginning on or after 1st January 2023.